ABSTRACT

The European Union must enhance four crucial factors for its future development: a) the existence of a high internal savings, b) a continuous growth in the demand of new “common goods” by the citizens in a service and knowledge economy, c) the continuous development of the excellence competencies by the workers and the enterprises, d) a consolidated history of cooperation at the European level. However, much of the domestic savings is invested in foreign financial assets, the needs of citizens are largely unsatisfied in the metropolitan areas and in the peripheral areas, unemployment especially of young people is too high and political tensions and fragmentation have increased within the individual countries and between the various European countries.

The increase in internal disparities, the slowdown in the European GDP growth and the new international challenges (migration, oil prices, trade wars, exchange rates and interest rates, etc.) indicate that a radical change is needed in the European macro-economic policies, both in the public budget and in the monetary policies. Therefore, this article illustrates the objectives and instruments of a new European industrial and regional policy. Higher growth is compatible with the financial balance at the European scale and with a rebalancing of the difference (€ 512 billion) between total internal investment and the algebraic sum of savings by public institutions, households, businesses and financial organizations in the various countries. All actors: governments, households, enterprises and banks can or must participate in a common strategy that enhances investor and consumer confidence, tangible and intangible investments and infrastructure in the territory and make use of the unused resources available in the different countries.

This article proposes the shift from an incremental approach to growth to a “disruptive” change in economic policy. Export is not enough to sustain growth and it is necessary to increase domestic demand and in particular internal investment, to reduce an unnecessary surplus of the external current balance and to launch joint investment projects by collecting the necessary financial and tax resources in an equitable manner among the various countries. Policies are needed that aim to stimulate and steer private and public investments towards new innovative productions and the development of knowledge, to invest in training, research and technical design, to increase productivity and wages, to stimulate the demand for new goods and services of high quality and for collective purpose and finally to develop the solidarity among the various economic stakeholders within the individual countries and to strengthen the mutual trust and the common European identity, creating a broad consensus among the various countries of the European Union for a strategy to be implemented together.

Investment in Europe could grow by 512 billions without compromising financial stability

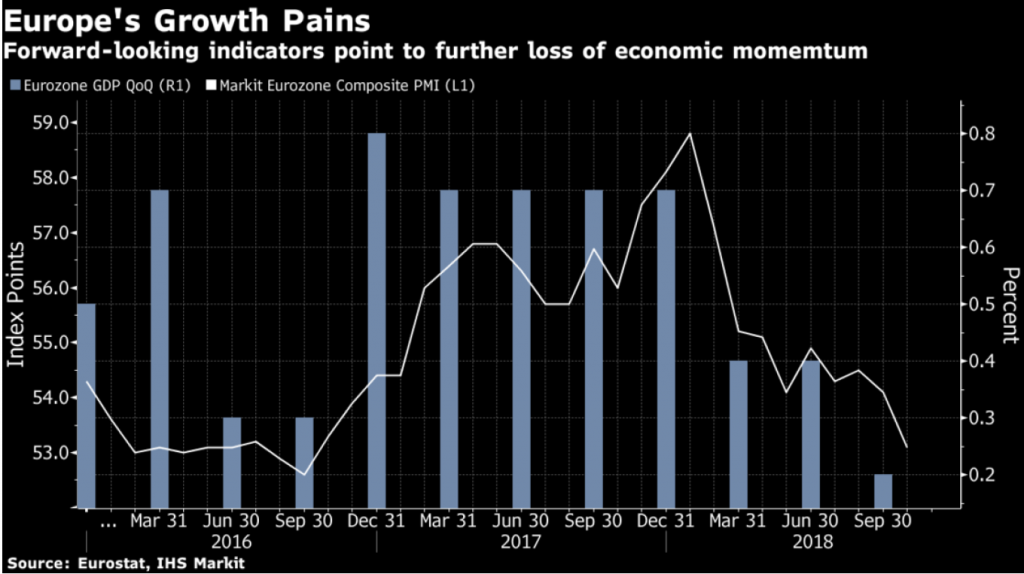

Economic growth in the European Union and in particular in the euro area after nine years from the financial crisis is still among the lowest in the world (2,4% in 2017, 2,0% in 2019 and 1,9% in 2010): both of the United States (2.2% – 2.9% – 2.5% respectively) and of emerging countries, such as China (6.9% – 6.6% – 6.2%, Source Imf World Economic Outlook: October 2018).

Moreover, the slowdown expected in 2019 in both the European economy and in most of the world economy requires also the start of new policies in the European Union and of course in Italy.

The German economy contracted for the first time since 2015 and in the third quarter 2018 the GDP contracted by 0.2 percent, which was worse than expected and larger in more than five years.

On the other hand, the GDP change in Italy with respect to the same trimester of the previous year according to Istat is decreasing since the first quarter of 2017 (1.7 percent) and it was only 0.8 percent in the third quarter of 2018.

The growth rate of industrial production with respect to the same month of the previous year fells in 2018 from 3.6 percent in April to 1.3 percent in September and the IHS Markit PMI® Composite Eurozone index in October in Italy was equal to 49.3 (minimum in 59 months, values lower than 50 indicate a decrease).

The unemployment in Italy, which had decreased in recent months, has returned to increase in October (2,613 mil. workers) and the unemployment rate is 10.1 percent and the young people unemployment rate is 31.6 percent: both among the largest in Europe and only smaller than in Greece and Spain.

Moreover, gross fixed investments in the euro area decreased by 1.5 percent during the 2007-2018 period and by 19.5 percent in Italy (Source European Commission, November 2018).

The future development of the European economy certainly depends on external challenges, such as the international migrations and the competition with large countries, such as the United States, China and Russia, but the factors of the economic and political crisis in the European Union are mainly internal and depend on the political instability of all European countries and of the EU institutions themselves. Moreover, they depend on the growth of social and economic disparities between countries and within each country, as well as an inadequate quality of the environment both natural and within the most congested urban areas .

The objective life conditions have deteriorated and do not indicate a prospect of improvement, especially for young people. Furthermore, the ever increasing levels of education and of free time lead citizens to demand an active participation in political decisions and to oppose more firmly the rigidity and arrogance of the “establishment” (governments, banks and large companies) at the national and international level.

The growing dissatisfaction for the policies of the European Union has led to the Brexit, to the electoral defeats of the center parties, to the electoral increase of populist parties, to the change of government majorities in almost all European countries in recent years. In general, the increase in disparities and the growing feeling of frustration are leading to a lack of trust, a growing nationalist closure, a lack of consensus on common objectives and the fragmentation of the European economy and society.

It is therefore necessary to change an economic policy approach that has led to these negative results and to define as soon as possible the guidelines of a program of the next European Parliament and of the European Union Commission in view of the next European elections in 2019.

The critique of the neo-liberal paradigm, dominant in the 1990s, and of the excessive power of the public and private, industrial and financial “establishment” is increasingly widespread, as they have been favoured by the economic policies of fiscal austerity and increasing liquidity and rescue of banks, privatization and indiscriminate deregulation and reduction of social services and of public investment.

Economic policies in Europe have focused on monetary policy measures, on the constraints to public budgets, on the labour market flexibility and on the other “structural reforms” and therefore have not focused their attention on the world of companies and on the factors that have led to a reduction in their investment propensity, as they have reduced the innovative capabilities and the long term productivity. This has led to neglecting the many factors, such as the change in business models of companies, in patterns of consumption by the citizens and in the forms of relationships between the different actors which are part of the national production and innovation systems. These factors are not directly modifiable with policies macro-economic and require appropriate industrial and regional policies.

Indeed, the continued increase of those who protest against austerity policies or even those who want to leave the Union (such as the United Kingdom and many “sovereignist” parties in other countries), indicates that there is a large gap between the European institutions and the electorate in the various member countries and have determined clefts in the popular consensus on favourite models of growth and forms of democracy. Therefore, it seems that it has arrived and it cannot be postponed the time for a change in European economic policy.

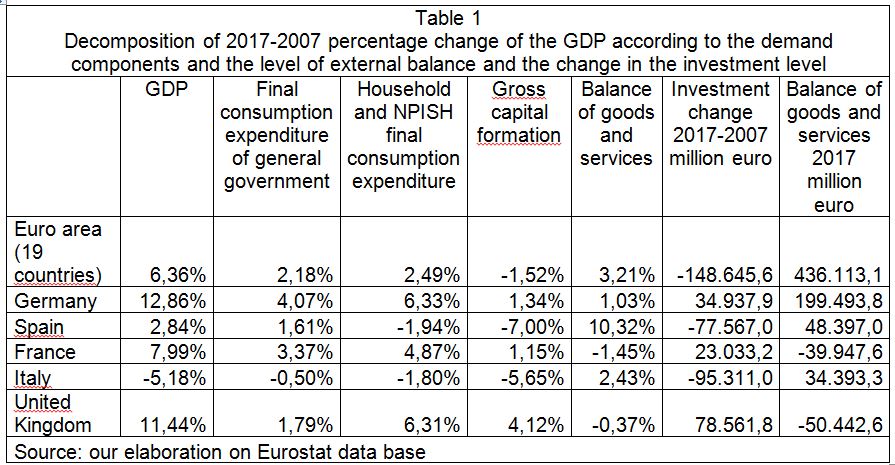

In the euro area, investment change in the 2007-2017 period was negative (-148 mil.). However, the balance of the current external balance was very positive in 2017 (€ 436 billion), as indicated in table1. That implies an outflow of financial funds from the euro area to the rest of the world, which could have instead been used to finance investment in the European Union. Therefore, the level of investments and the corresponding level of domestic demand could be much higher, without determining a deficit in the external balance. In particular, the level of investment could have been much higher in Germany, Italy and Spain, thus allowing an increase of the of GDP growth rate. On the contrary, in the case of France and the United Kingdom, investment growth in 2017 compared to 2007 was supported by a current account deficit, which certainly contributed to the higher GDP growth rate of these countries compared to the Italy and Spain, where austerity in public budgets and the leverage reduction policy of private companies have had a negative impact on GDP growth.

The “mercantilist” policy aimed at expanding exports rather than the domestic demand of the European economy and in particular of some countries (Germany, the Netherlands and Italy) has aimed at promoting the international competitiveness of firms in the short term, rather than the increase in wages, disposable income, consumer demand and the propensity to invest and innovate. In fact, the austerity policies of public budgets and the high taxation of households and capital gains have been the cause of a structural imbalance between domestic demand and supply, as they have reduced internal investments and consumption, both private and public.

Therefore, a priority in European economic policy should be to reduce the excessive surplus of the euro area’s overall current balance, which is the largest in the world and even higher than that of China, in order to restore the equilibrium between internal demand and aggregate supply or between internal savings and investments.

The need to pursue this objective in European policies was initially proposed in e-book published by the Discussion Group “Growth of investments and territory” (2017: https://economia.uniroma2.it/dmd/crescita-investimenti-e-territorio ).In particular, that is relevant now in the discussion on the “long-term European budget” and on the annual European budgets in the next years 2018-2020. This also implies a change in the European parameters used to assess national public budgets.

In fact, the recent European Commission (Autumn 2018) forecasts for 2018 and 2019 are “neutral” forecasts with an unchanged policy (or based on the already announced policies by the governments for 2019, which are analogous to those in previous years) while very different results would be possible if more appropriate economic policies were made at the European level. Indeed, the current deceleration in European growth could be effectively countered by an appropriate European industrial policy strategy that would boost private and public investment without compromising financial stability.

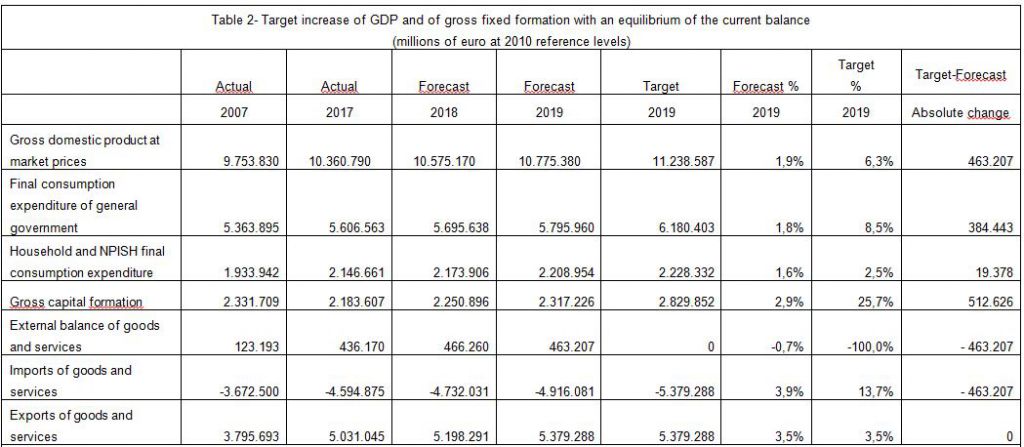

In particular, the macroeconomic implications for the euro area economy of new economic policies can be illustrated by a numerical example, as shown in Table 2. In fact, if exports are considered as fixed, it would be possible to increase domestic demand and imports by a value exactly equal to the expected positive current balance in 2019 and this would lead to an increase in GDP in 2019 of the same amount. Therefore, domestic demand and imports could increase without compromising the external financial stability or the balance between exports and imports of the European economy.

The estimate shown in Table 2 is based on the assumption that the GDP shares of private and public consumption could be the same as in the 2017 reference year. Therefore, investments could be increased up to a level equal to the difference between the new level GDP target and the sum of private and public consumption.

According to these calculations, the growth rate of GDP in 2019 in the euro area could be 6.3 percent and therefore higher than 1.9 percent indicated in the European Commission forecasts in autumn 2018 or the GDP could grow by 463 billion. In particular, investments in the euro area could be EUR 512 billion higher than those currently forecast for 2019 and therefore increase by 25.7 percent compared to the level of investments in 2018 and could be kept constant at this level in the subsequent years without compromising the balance of the external current account. Even the growth rate of private consumption (8.5 percent) and that of public consumption (2.5 percent) could be much higher than that in the forecast by the European Commission for 2019.

Source: elaboration by R. Cappellin (2018) on data: European Commission Economic and Financial Affairs AMECO (Last Update 8 November 2018), http://ec.europa.eu/economy_finance/ameco/user/serie/ResultSerie.cfm

This estimate is based on a solid economic theory such as the Thirlwall model (1979), according to which the guaranteed GDP that insures the equilibrium in the trade balance is determined by the level of exports and by the propensity to consume and import:

ΔX = (m c) * ΔY

where (m) is the propensity to import and (c) the propensity to consume, (X) are exports and (Y) is GDP. Compared to the Thirlwall model, the estimate in Table 2 is much more conservative, and the results are certainly inferior to reality, since it is based on the certainly limiting a propensity hypothesis that the import (m) is equal to one or that the whole increase of GDP would lead to more imports, while in reality a large part of the increased aggregated demand would be produced internally. Moreover, this simple estimate assumes that the multipliers of consumption and of investment are equal, while investments may have a higher multiplier.

Clearly, a limitation of the above calculation is that it assumes that unused production capacity in the euro area is high and that it is possible to increase domestic production, by increasing productivity and employment, so as to cope with the increase of domestic demand and GDP. This certainly seems possible, given the high number of unemployed in the euro area and the fact that the increased investment and the induced innovations would certainly increase the potential GDP.

Therefore, the estimate presented in Table 2 shows that the euro area could significantly increase investment, and therefore domestic demand and GDP, without compromising external financial stability of the European Union or continuing to live “within the limits of its own resources”, unlike what actually happens not only in the United States, but also in European countries such as France and the United Kingdom, which have a high negative external balance. The increase in the future growth of investments and productivity represents for the European Union a more solid political objective than to maintain an excess of savings on investments, determining the accumulation of financial assets abroad and a low level of material investments and intangible assets and of domestic demand.

This estimate was developed by the Discussion Group “Growth, Investment and Territory”, which is an independent “cross-party” think-tank, which combines many well-known economic and no economic experts and aims to explore the impact of research on economic politics and institutions and to promote and improve public policies. In recent years, the Group has developed a series of publications, in which the characteristics of a new European economic policy are indicated in a precise and operational manner, aimed at promoting innovation, investment, quality of life in European cities and in territory and in which the growth of the European economy is driven by domestic demand (Gruppo di Discussione 2017 and 2018).

Clearly such a policy requires that the most developed countries in Europe, in which there are the most innovative productions and enterprises (“disrupters”), should be the first to start this new cycle of development, so that the recovery can then be extended to the countries at an intermediate level of development, which certainly alone would not be able to act in countertendency, but can only play the role of “multiplier” of the initial impulse. It is also true that in countries with less development such as Italy, governments have so far shown that they are not aware of the possibility of a new growth strategy and therefore have not been able to make adequate proposals for a different policy to the European Commission.

It is therefore necessary to move from an incremental approach of economic growth to a “disruptive” change in national and European economic policy due to the speed of innovation processes that currently occur in all productions. In fact, economic development is not due to incremental growth in the same companies, the same sectors and territorial areas, but requires it an acceleration of structural change.

Due to the economic development and the increasing levels of income, levels of education and even the increase in the free time for the citizens, there is a growing need for services for collective interest addressed not only to the individuals but to groups of citizens. These services enhance the relationships of interdependence in consumption between different individuals and the cross-industry interdependence between many sectors. Such assets are defined differently by the economic theory, such as: public goods, common goods, club goods or relational goods.

According to the definition of public goods in economic theory (the conditions of non-exclusion and non-rivalry), goods can be defined as “common goods on a European scale” when the network externalities and the homogeneity of preferences are crucial, even more than the neoclassical concept of economies of scale (“vertical subsidiarity”). Therefore, European intervention should focus on those goods that have a specific “community added value”, such as: cultural heritage, knowledge, culture, the urban and natural environment, that can be shared by all European citizens. In general, it is necessary that the joint action by the European institutions together with that of national and regional governments aims to meet the needs by of European citizens of housing, leisure and culture, economic growth and employment, training and health, environmental sustainability. In particular, it is a still unsatisfied need by the citizens, that of a prospect of future economic progress and of a balance between a strong collective identity and the autonomous individual differentiation. Therefore, collective needs are also those of political participation, social solidarity towards the weakest, of justice, of fight against corruption and of security.

Therefore, the relaunching of the European economy must start, first of all, from the identification of the new needs of citizens in an economy of services and knowledge and the existing opportunities for the development of new productions, aimed at satisfying these needs. The objective of European economic policies must be to ensure that all citizens and not only the rich and/or the residents in large metropolitan areas, but also the poorest citizens and those living in the different peripheral regional areas, can enjoy a quality of the life that is comparable to that enjoyed by the richest citizens and the most prosperous countries and regions.

It is necessary that the public budgets of the individual States and of the European Union provide for adequate public investments and tax and financial incentives for private investments, both in infrastructures and machinery, as well as in basic and continuous research and training, for the creation of new productions, more jobs especially for young people and women, a strengthening of university and specialist training, an improvement in health, transport, energy conservation, the protection of historical and cultural heritage, the natural environment and the defence of the territory against natural disasters. It is necessary that the policy of innovation and investment or the industrial policy in the broad sense not only promotes the supply by companies and the public sector, but also the demand by the citizens for new goods and services of a collective nature, taking into account the different specificities of the countries and the territory considered.

The model of the “globalization”, based on the free circulation of goods and capital, and of the “free enterprise”, as well as the opposite model of “localism / sovereignism”, both limit the economic integration between the various countries and are inadequate in a modern knowledge society, where the process of interactive learning is important between individuals and the local communities even of different countries, and therefore very close forms of economic integration on an international and interregional scale are necessary.

In conclusion, the European Union must not only aim at “negative/defensive” objectives, such as preventing internal conflicts, defending against external dangers or reducing obstacles to the free movement of goods, services, capital and people, but it must also act in a “proactive” way and aim to achieve common objectives, initiate joint investment projects and collect the required financial and tax resources in a fair way among the different countries.

Finally, it is necessary to promote a broad consensus among the various countries of the European Union on a common strategy, to be implemented together. In fact, the European Union is subject to enormous challenges and tensions and this would require common policies to strengthen its common identity, which concerns the sense of common belonging of European citizens and the sharing of common social and cultural values. This is a prerequisite for strengthening the European institutions, as it is necessary to undertake joint actions aimed at a more courageous sustainable future by the various countries. Furthermore, in order to ensure greater citizen participation in political decisions, a policy of institutional reform is needed that regulates the powers of the different levels of government and between the public and private sectors (“multilevel governance”).

References

Article by Riccardo Cappellin[1], Maurizio Baravelli[2], Enrico Ciciotti[3], Enrico Marelli[4] and Luciano Pilotti[5]

Contacts

Discussion Group “Investment Growth and Territory”

[1] University of Rome “Tor Vergata”

[2] University of Rome “Sapienza”

[3] Catholic University Cattolica of Piacenza

[4]University of Brescia

[5] University of Milano